How Parcel Shipping Insurance Impacts Every RFP You Submit

When a shipper’s procurement team opens your RFP response, the cargo protection section now carries as much weight as your rates and transit times. Answer with “carrier liability” and a generic promise to “support claims,” and you signal limited risk management maturity, especially to shippers in e-commerce, medical devices, pharmaceuticals, collectibles, and industrial B2B.

A tech-enabled, all-risk parcel insurance program with API integration and a white-labeled claims portal tells a different story. It says that your organization manages risk proactively, protects your clients’ revenue, and delivers an enterprise-grade experience.

This post explains what sophisticated shippers are now looking for in a parcel insurance program, why coverage gaps drive silent churn, and exactly what your RFP responses need to demonstrate to win.

The stakes have never been higher for parcel protection

Parcel protection has become an RFP decision factor

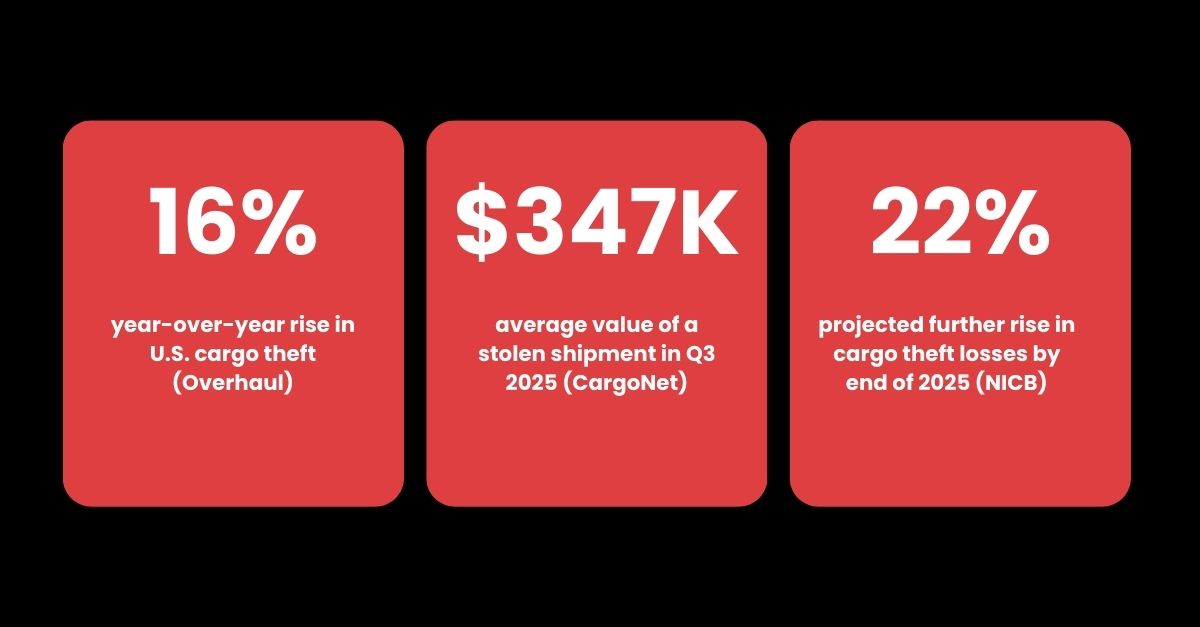

Cargo theft rose 16% year-over-year in the U.S. in 2025, with the fourth quarter accounting for 30% of annual incidents. The average value of a stolen shipment reached $347,334 in Q3 2025, more than double the prior year’s figure.

Against that backdrop, C-suite buyers at e-commerce brands, medical device manufacturers, pharmaceutical companies, trading-card and collectibles marketplaces, and auto-parts distributors are no longer treating shipping insurance as boilerplate fine print tucked at the end of a master service agreement. They ask how well their goods are protected, how quickly claims get resolved, and who owns the experience when something goes wrong. And they are increasingly formalizing those questions inside RFPs.

An LSP that still relies just on carrier liability looks like a commodity broker, not a strategic partner. On the other hand, one that offers comprehensive, tailored shipping insurance stands out immediately.

“For parcel shippers, the way you handle a claim is the moment they decide whether you’re a vendor or a partner.”

For a deeper dive into why all-risk coverage outperforms carrier liability and named perils policies, see: Why All-Risk Cargo Insurance Matters for LSPs.

What shippers actually evaluate in an RFP

When procurement teams at mid-market and enterprise shippers compare LSPs, they don’t just ask “Do you have insurance?” They evaluate how the program behaves in the real world. Four criteria surface in RFPs and follow-up conversations.

1. What coverage type do you offer: carrier liability, named perils, or all-risk?

Carrier liability is not insurance. It is a limited obligation, often tied to weight-based formulas and carrier negligence, with strict exclusions and low caps that rarely match the actual value of modern shipments. Named perils policies add protection only for specific, listed causes of loss. If the peril, like porch piracy, mysterious disappearance, or last-mile theft, isn’t named, the claim is denied. Shippers discover this the hard way.

All-risk shipping insurance does the opposite by covering all causes of physical loss or damage except those specifically excluded, such as inherent vice or improper packaging. For parcel-heavy LSPs, an all-risk program covers virtually any commodity, route, and carrier — including the high-risk scenarios that carrier liability routinely excludes. In an RFP, “all-risk shipper’s interest coverage matched to declared value” reads as a concrete advantage.

2. How transparent and fast is your claims process?

From the shipper’s perspective, a claim is the moment the relationship goes on trial. Under carrier-by-carrier liability processes, a team must gather invoices, photos, and statements, then submit claims through dozens of different portals or email workflows, each with its own forms and timelines. This typically results in slow responses, inconsistent documentation requirements, and elevated denial rates, especially for porch piracy and last-mile scenarios.

A tech-enabled all-risk program replaces that patchwork with a standardized, digital claims experience. Shippers can submit claims through a white-labeled portal, receive a claim number immediately, upload documents in one place, and check status in real time while communicating directly with a claims adjuster. Once documentation is complete, typical adjustment times can be 5–7 days, not months. In an RFP, being able to cite specific timelines and portal capabilities is a powerful differentiator.

3. Is your insurance program integrated into your technology stack?

Sophisticated shippers expect their parcel partners to operate like true platforms, not manual middlemen. That expectation now extends to cargo protection: they want coverage to bind automatically when a shipment is tendered, premiums to calculate based on shipment parameters, and policy data to flow into the same systems where they track orders.

With an API-driven all-risk solution, an LSP can embed rating, binding, and voiding directly into its own TMS or customer-facing portals. Shipment details like value, destination, mode are passed via API; coverage attaches in real time; and insurance activity is recorded centrally across warehouses and carriers. In RFPs, this looks like a diagram of your workflow instead of a vague statement that “insurance is available upon request.”

4. Does the claims experience reinforce your brand, or hand clients off?

Every RFP implicitly or explicitly talks about customer experience, but very few LSPs extend that thinking into the claims process. When a shipper has to exit your systems, call carriers individually, and wrestle with unfamiliar third-party portals, your brand disappears at the exact moment they need you most.

A white-labeled claims portal keeps your identity front and center, even though a specialist partner handles the complex work behind the scenes. For C-suite buyers, that level of brand continuity is an unmistakable signal of operational maturity and long-term commitment.

The coverage and claims gap shippers have already noticed

Many LSP executives still object: “Our customers don’t ask about insurance in RFPs, so it can’t be that important.” The reality is harsher. Shippers often don’t argue about coverage until after a claim goes badly, and even then, they may not escalate. They simply move their business at renewal.

This is where silent churn shows up. An account that looks healthy on your scorecard may already be exploring alternative 3PLs because of one bad claims experience. When those shippers run their next RFP, they ask sharper questions about coverage type, claims timelines, and brand.

Carrier liability’s restrictive terms create pain points shippers remember long after the paperwork is done: limited recovery based on weight rather than sales price, exclusions for porch piracy or unattended deliveries, and inconsistent rules by geography. A medical device maker that recovers only a fraction of a damaged shipment, or a trading-card merchant whose porch-piracy claims are repeatedly denied, carries that frustration directly into the next RFP cycle.

An account that looks healthy on your scorecard may already be exploring alternatives — because of one bad claims experience.

Case study: how a global omni-channel 3PL turned parcel insurance into a competitive edge

A global omni-channel 3PL — providing fulfillment for thousands of brands from more than 30 warehouses across the U.S., U.K., EU, Canada, and Australia — illustrates exactly how parcel insurance can reshape both operational performance and RFP competitiveness.

Before: carrier liability, fragmented claims, mounting friction

The 3PL relied on carrier liability and manually handled claims with each carrier individually. Its team spent enormous time collecting claim data, photos, and invoices from thousands of merchants, then filing across disparate carrier systems with different forms, documentation requirements, and timelines. Coverage was constrained by strict negligence standards and low limits, leading to high denial rates on issues like porch piracy. The result: a bottlenecked internal process, frustrated merchants, and difficult conversations every time coverage gaps surfaced.

After: a standardized all-risk program and white-labeled claims portal

The 3PL implemented a customized, end-to-end all-risk insurance solution managed through Cabrella’s native software platform. The program standardized coverage for virtually any commodity and transit route, with API parameters that let the 3PL embed rating, binding, and voiding directly in its own brand-facing systems.

For claims, the 3PL deployed a two-tier system: staff could file on behalf of merchants, and merchants gained access to a custom, white-labeled claims page with advanced self-service features, status tracking, document upload, and structured checklists.

The outcome: efficiency, transparency, and competitive differentiation

By introducing the white-labeled self-service portal, the 3PL shifted roughly 70% of claim-filing workload away from its internal team to merchants and a specialist subrogation partner. Claims were reorganized into structured reports, enabling more effective subrogation with carriers and better visibility into loss metrics by carrier, warehouse, and brand.

Merchants gained comprehensive insurance covering sales price (including shipping and tax) for a wide range of commodities and routes, with higher approval rates, faster turn times, and coverage for porch piracy and other previously excluded risks. The 3PL now positions this as a competitive edge in every RFP — combining a user-friendly tool, comprehensive coverage, and enterprise-grade brand continuity.

Read the full Cabrella case study.

What your parcel insurance offering must demonstrate in every RFP

Use the following checklist as a self-assessment. If you can’t check every box, your parcel insurance response has a gap your competitors can exploit.

Ready to win more business with your parcel insurance offering?

See what all-risk parcel insurance looks like inside an RFP response — and how to implement it in your service offering. Check out Cabrella's capabilities, review the full case study, and learn how LSPs of every size are turning shipping insurance into a competitive advantage.

Subscribe for Email Updates